Understanding How Your Benefits Are Taxed

Social Security benefits are a critical part of retirement income for millions of Americans. But one of the most commonly misunderstood aspects of receiving these benefits is taxation. Many people assume that once they’ve paid into Social Security, they won’t have to pay taxes on the benefits they receive. Unfortunately, that’s not always the case.

In this guide, we’ll walk through the history, the current tax rules, and the most important things you need to know about how your Social Security benefits may be taxed.

Social Security benefits weren’t always taxed. In fact, from the creation of the program in 1934 until 1979, benefits were completely tax-free.

That changed when concerns began to rise about the long-term sustainability of the Social Security Trust Fund. In response, a presidential commission (later known as the Greenspan Commission) studied the issue. Their findings led to a major legislative change:

These two milestones form the basis for the taxation rules that are still in place today.

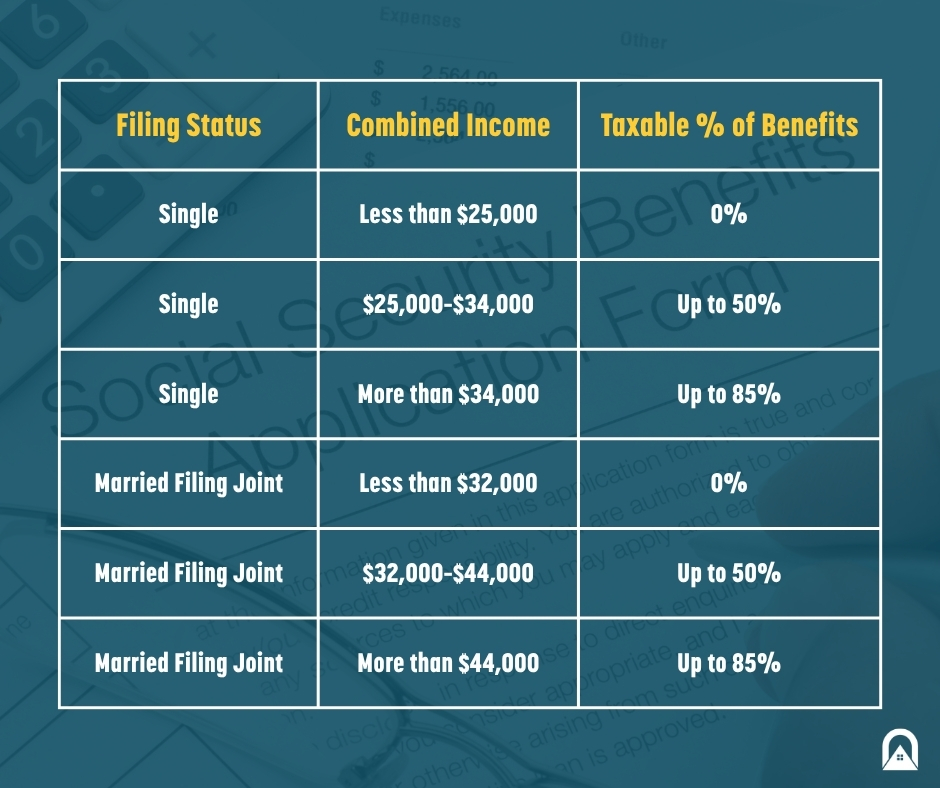

Social Security benefits are not taxed like regular income. Instead, whether your benefits are taxed—and how much—is determined by your "combined income."

Combined income is calculated as:

Adjusted Gross Income (AGI) + Nontaxable Interest + 50% of Your Social Security Benefits

These thresholds have not been adjusted for inflation, meaning more retirees are subject to taxation every year.

How we got this couple $112,000 more in social security income.

You might wonder: why not just treat Social Security like any other income and tax all of it?

The answer lies in how the system is funded.

Social Security is funded through:

Since you already paid taxes on your earnings when they were first collected for Social Security (via payroll taxes), taxing the entire benefit again would be considered double taxation. That’s why only 50% to 85% of your benefits can be considered taxable income—depending on how much other income you earn.

❌ Misconception: “If I get Social Security, I’ll always pay taxes on it.”

✅ Truth: Not necessarily. Many lower-income individuals or retirees who don’t draw from other taxable sources may have little or no tax on their benefits.

❌ Misconception: “The income means test and the tax formula are the same.”

✅ Truth: These are completely separate rules. The income-related monthly adjustment amount (IRMAA) is a Medicare premium surcharge based on income. It is not the same as Social Security income taxation.

What happened to Social Security in 2025? We’ve reviewed all 2025 changes to Social Security here.

Understanding how your Social Security will be taxed helps with retirement income planning. Here are some steps to consider:

Social Security taxation is not simple, but understanding the income thresholds and the reasons behind the tax structure can help you make smarter decisions about retirement planning.

You worked hard for your benefits. Make sure you also understand how they’ll affect your tax bill.

Disclaimer: This post is for informational purposes only and does not constitute tax advice. Always consult with a CPA or licensed financial advisor for your specific situation.

We are in the business of helping people like you retire happily ever after, no matter your net worth. So, if you are looking to maximize your benefit, having a hard time navigating the system, or are simply confused by the tax question, we want to help. You can book your 100% free consultation here.

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur.

Block quote

Bold text

Emphasis