Social security is a fundamental part of your plan, but the important thing to remember is that this is your retirement and your plan.

Retirement planning is often painted as a numbers game—save enough, invest enough, and hope that it all works out when the paychecks stop coming in. But the truth is that successful retirement planning isn’t about amassing a mountain of assets; it’s about creating a strategic plan for income. Social Security is the cornerstone of this plan, yet few people realize how much is left on the table simply by claiming benefits without a thoughtful strategy.

This guide dives deep into how Social Security optimization, careful use of retirement savings, and low-risk investments can extend your wealth and create a retirement that’s not just comfortable but enjoyable. Drawing from real-world examples, we’ll explore strategies that can mean hundreds of thousands of dollars in difference over the course of your retirement.

Table of Contents:

For many Americans, Social Security is the single most important retirement benefit they’ll receive. The average couple approaching retirement can expect to receive a combined benefit that covers a significant portion of their monthly expenses, particularly if they optimize their claiming strategy.

However, most people still claim benefits too early. Many financial advisors default to the idea of claiming at the earliest age—62—or at full retirement age (FRA), which is between 66 and 67, depending on your birth year. While these strategies may feel “safe,” they often leave substantial money on the table.

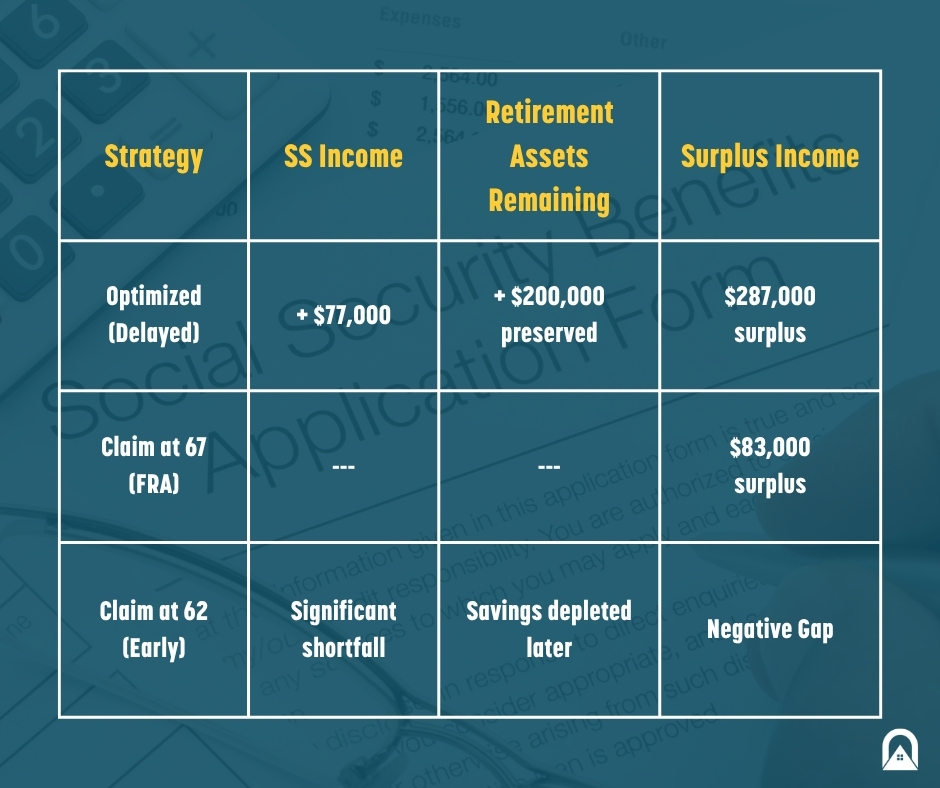

Let's talk about a powerful case study involving a married couple—David and Celeste—who optimized their benefits by waiting. Instead of filing early, David delayed until age 70, while Celeste claimed at a strategically timed moment. This approach not only gave them $77,000 more in Social Security income but also allowed them to preserve $280,000 in retirement assets that would otherwise have been spent.

The temptation to claim early often stems from fear. People worry that Social Security might run out, or they feel they “deserve” to claim benefits as soon as possible after working decades. But claiming early permanently reduces your monthly benefit and leaves you with fewer resources as you age.

Consider three approaches:

The difference between claiming early and delaying can easily exceed $100,000 in lifetime benefits for many couples, especially when inflation is factored in.

Social Security should form the bedrock of your retirement income, but it’s just one part of the puzzle. The right plan allows your retirement accounts—such as 401(k)s, IRAs, or pensions—to become tools for enjoyment, not just survival.

Start by calculating your basic retirement lifestyle costs:

David and Celeste, for example, determined they needed about $5,000 per month to maintain their lifestyle in Southeast Florida. This gave us a baseline to design a plan where Social Security would cover as much of this amount as possible.

Once you know your expenses and have an estimate of your Social Security and pension income, calculate the “gap.” This is the shortfall between your guaranteed income sources and your needs.

For David and Celeste, there was a five-year window between David’s retirement (age 65) and when he began claiming Social Security (age 70). During this period, they used a small portion of their retirement savings to cover the gap, allowing their Social Security benefits to grow to their maximum potential.

Many retirees instinctively draw from their savings first and claim Social Security early. This approach might feel comfortable, but it reduces the longevity of your savings and forces you to rely on uncertain market returns.

David and Celeste flipped this script:

This demonstrates a key point: the order of withdrawals matters as much as the amount.

WE suggested placing a portion of their unused retirement funds—about $265,000—into a fixed-rate account earning 6% annually, similar to a bank CD but with tax-deferred growth. By age 70, that account grew to $357,000, providing a “fun fund” for travel, hobbies, or emergencies.

This approach contrasts sharply with big investment firms that often push clients toward fee-heavy portfolios, which can erode savings. As noted, a 2% annual fee on a $100,000 portfolio over 20 years can result in $100,000 in lost fees—essentially giving away your savings to your advisor.

Inflation is an unavoidable reality of retirement. A monthly benefit that seems sufficient today may fall short in 10 or 20 years. Social Security is one of the few income sources that is adjusted for inflation each year. By delaying benefits, you not only start with a higher base amount but also receive larger COLA increases.

For example, if David and Celeste had claimed at FRA, they would have needed to draw more from their savings each year to keep up with rising costs. By waiting, they ensured that Social Security covered nearly all expenses, adjusted for inflation, freeing up their investments.

One of the most common misconceptions in retirement planning is the focus on “how big your nest egg is.” People obsess over having $1 million or $2 million in their accounts, believing this number alone guarantees security. The truth is, income streams matter more than lump sums.

David and Celeste illustrate this shift perfectly:

If you have multiple income sources—such as a pension, IRA, or annuity—you need to coordinate them with your Social Security claiming strategy. For David, an $800 monthly pension supplemented the delayed Social Security benefit, providing another layer of guaranteed income.

It's clear that many retirees make preventable mistakes that cost them thousands:

Let’s look at David and Celeste’s outcomes side-by-side:

The optimized strategy not only increased income but also created flexibility for their savings to grow.

If you’re within 10 years of retirement, now is the time to create a detailed plan. Here’s how to start:

Social Security is just one piece of the puzzle. Healthcare costs are often the biggest expense in retirement. Coordinating Medicare enrollment (typically at age 65) with your Social Security strategy is essential. A smart plan accounts for:

David and Celeste’s plan included Medicare coverage, ensuring that unexpected medical bills didn’t derail their strategy.

CHECK OUT OUR GUIDE TO MEDICARE

Not all financial advisors operate in your best interest. Large firms often require minimum assets (e.g., $500,000) before even considering your case, because their focus is on managing investments for fees—not on optimizing guaranteed income sources like Social Security.

Look for:

Ultimately, retirement isn’t just about numbers—it’s about life. A solid plan means you can travel, pursue hobbies, and spend time with family without constantly worrying about whether you’ll run out of money.

David and Celeste now have:

Learn about how Dave and Judy Got $112,000+

“If you’re within 10 years of retirement and you can afford to throw $300,000 away, skip this video.” It’s provocative, but it’s also true. Without a strategic plan for Social Security and income management, you could unknowingly lose hundreds of thousands of dollars.

Retirement planning is not about luck or timing the stock market. It’s about making smart, informed decisions with the resources you have—decisions that ensure your income lasts, your savings grow, and your retirement is everything you want it to be.

Book your FREE consultation and let’s get you set up for a happy retirement.

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur.

Block quote

Bold text

Emphasis